Picking the right 529 plan investments doesn’t have to feel overwhelming. Most college-savings plans funnel your contributions into one of three familiar portfolio styles—age-based, static allocation, or single-fund. When we match each option to your child’s years until college and to your comfort with market swings, we give the account a clear path to tax-advantaged growth.

Three common types of 529 portfolios

Most plans group their investment menus into three familiar buckets — age-based tracks, fixed (static) mixes, and single-fund options — so you can match risk to your timeline and comfort with market swings.

Most plans group their investment menus into three familiar buckets — age-based tracks, fixed (static) mixes, and single-fund options — so you can match risk to your timeline and comfort with market swings.

1. Enrollment or age-based portfolios

Think of these options as autopilot tracks. When your child is younger, the glide path leans heavily on stocks for growth, roughly 60 percent stocks and 40 percent bonds in Missouri’s MOST 529 plan Moderate track for kids under age five. By the time college is around the corner, that mix shifts toward safety; the same track holds about 10 percent stocks and 90 percent bonds at age eighteen, with cash-like reserves ready for withdrawals. This set-it-and-adjust design suits families who would rather not tinker with allocations every few years.

2. Static allocation portfolios

2. Static allocation portfolios

A static choice locks in one mix of stocks and bonds on day one and keeps that blend until you decide to move. For instance, Utah’s my529 plan offers an 80/20 Aggressive track, a 60/40 Balanced track, and a 20/80 Conservative track, figures that describe how each dollar splits between equities and fixed-income investments. You pick the profile that matches your appetite for volatility, then let the plan handle rebalancing inside that fixed ratio. If you’re not sure which mix fits you, tools on many plan websites can help translate your comfort level into an actual portfolio. Bright Start 529 offers a risk-tolerance questionnaire and an investment-portfolio comparison tool called the Bright Start 529 College Savings Plan Portfolios that walk Illinois families through their options before they choose among its static allocation portfolios, outlining each mix’s fees, asset breakdown, and Morningstar-tracked performance. If your comfort zone changes later, most 529 plans still let you switch to a new static mix twice per calendar year.

3. Individual or single-fund portfolios

These options place every dollar in one underlying fund, giving you Lego-block control over the account. Want pure stock exposure? Virginia’s Invest529 Total Stock Market Portfolio invests 100 percent in the Vanguard Total Stock Market Index Fund and charges a 0.063 percent expense ratio. Prefer stability? Illinois Bright Start offers a Principal Plus Interest portfolio that credits a 3.00 percent annual rate for the 2025–26 period, backed by a TIAA-CREF Life funding agreement. By mixing these single-fund pieces — or adding one to an age-based track — you can dial your child’s 529 college savings plan toward the exact risk or return profile you have in mind.

Matching portfolios to your time horizon

The shorter the runway to tuition bills, the more cushion we usually want. Here is a data-backed way to think about it:

- More than 10 years out

Vanguard’s Target Enrollment 2044/45 portfolio — roughly for toddlers today — holds 95 percent stocks and 5 percent bonds, maximizing growth potential while college is still a decade or more away. - About 5–10 years out

By the time your child is in middle school, a mid-range option like Vanguard 2034/35 has already dialed back to 57 percent stocks and 43 percent bonds, striking a balanced posture. - Less than 5 years out

With freshman year around the corner, capital preservation counts most. Vanguard 2026/27 sits at just 18 percent stocks, 45 percent bonds, and 37 percent cash-like reserves, cushioning short-term market swings.

No mix can erase risk entirely, but tying your 529 plan’s stock exposure to the calendar — and adjusting only when life circumstances change — keeps the account’s risk level in step with your deadline.

Considering your personal risk tolerance

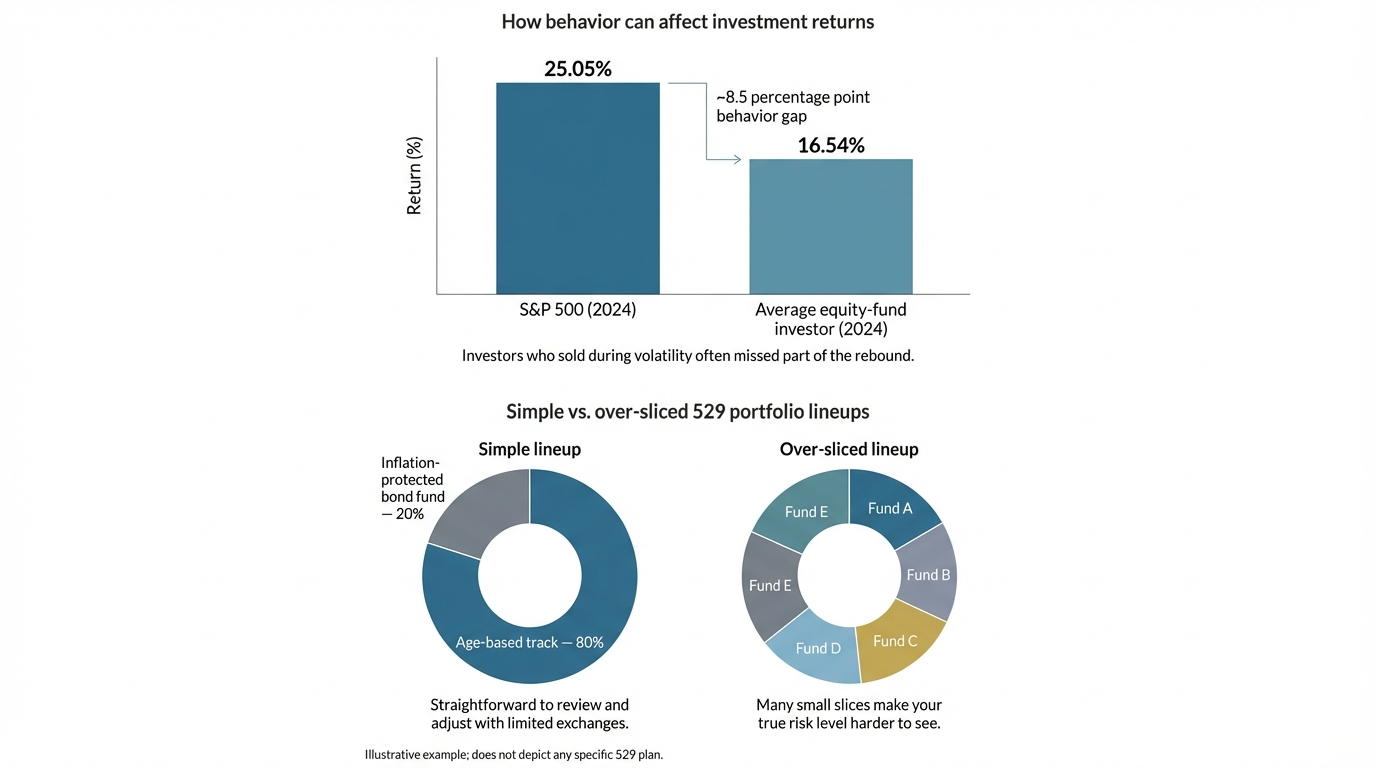

Timeline is not the whole story; your comfort with market swings matters just as much. In 2024, the average equity-fund investor captured only 16.54 percent, while the S&P 500 gained 25.05 percent. That eight-percentage-point behavior gap appeared because many investors sold during alarming headlines and missed the rebound.

If you lose sleep when stocks dip, anchoring your 529 plan in a slightly more conservative mix can keep you invested through rough patches. Conversely, if you can shrug off short-term declines in pursuit of higher growth, leaning on a stock-heavier portfolio early on may serve you better. The key is choosing a strategy we can stick with, changing course only when your goals or timeline truly shift, not when the news cycle does.

If you lose sleep when stocks dip, anchoring your 529 plan in a slightly more conservative mix can keep you invested through rough patches. Conversely, if you can shrug off short-term declines in pursuit of higher growth, leaning on a stock-heavier portfolio early on may serve you better. The key is choosing a strategy we can stick with, changing course only when your goals or timeline truly shift, not when the news cycle does.

Combining portfolios thoughtfully

We can mix and match 529 plan options, but moderation is key. A common tactic is to keep about 80 percent of the account in an age-based track for automatic glide-path adjustments and place the remaining 20 percent in a single-fund inflation-protected bond portfolio to soften volatility. Because the IRS allows only two exchanges of existing 529 assets per beneficiary each calendar year (savingforcollege.com), keep the lineup lean enough to make meaningful changes later if goals shift. Too many small slices, such as five funds each holding less than 10 percent, make it tough to judge your true risk level and may exhaust those limited reallocation windows sooner than expected.

Conclusion

According to savingforcollege.com, the IRS lets us rebalance a 529 plan’s existing assets only twice per calendar year, or whenever we change the beneficiary on the account. That guardrail keeps most families from tinkering too often, yet a yearly check-in still makes sense. Good reasons to act include:

- Your timetable moves, perhaps a gap year disappears and freshman year is suddenly twelve months away.

- Your personal safety net shrinks or grows, changing how much risk you can accept.

- Your lineup has sprawled into too many slivers, making the overall mix hard to read.

Outside those cases, resist the urge to tweak just because markets zig or zag. A once-a-year review, ideally on the same weekend you update other financial tasks, confirms that your 529 plan’s risk still fits your timeline and temperament. If it does, stay the course and keep contributing; consistency, more than perfection, is what builds a well-funded path to college.