Sub-Saharan Africa is predicted to have a housing shortfall of 50.5 million units. Every government has identified residential housing as a critical issue, yet it still needs to be resolved. It appears to be an insurmountable challenge, particularly for “social housing.” The banks of Africa are unwilling or unable to give mortgages at the appropriate volume. Underwriting competence and/or regulatory motive need to be improved.

Challenges with the housing

Housing projects (especially those created by foreign businesses) frequently fail to target the necessary market groups. Not focusing on middle-income or “social housing” (less than $25,000). Inconsistent or low-quality building. Lack of international-level building trades training (for example, concrete mixing, roof installation, and finishing). Scale economies of scale are limited. House building is frequently a project overseen by the owner or a representative of the owner. Cost overruns are not uncommon. With a lack of faith, many Africans have been “swindled” and no longer believe that a firm would produce a decent house as promised. Financing is unavailable. Most nations have no or highly restricted mortgage markets.

Probable Solutions

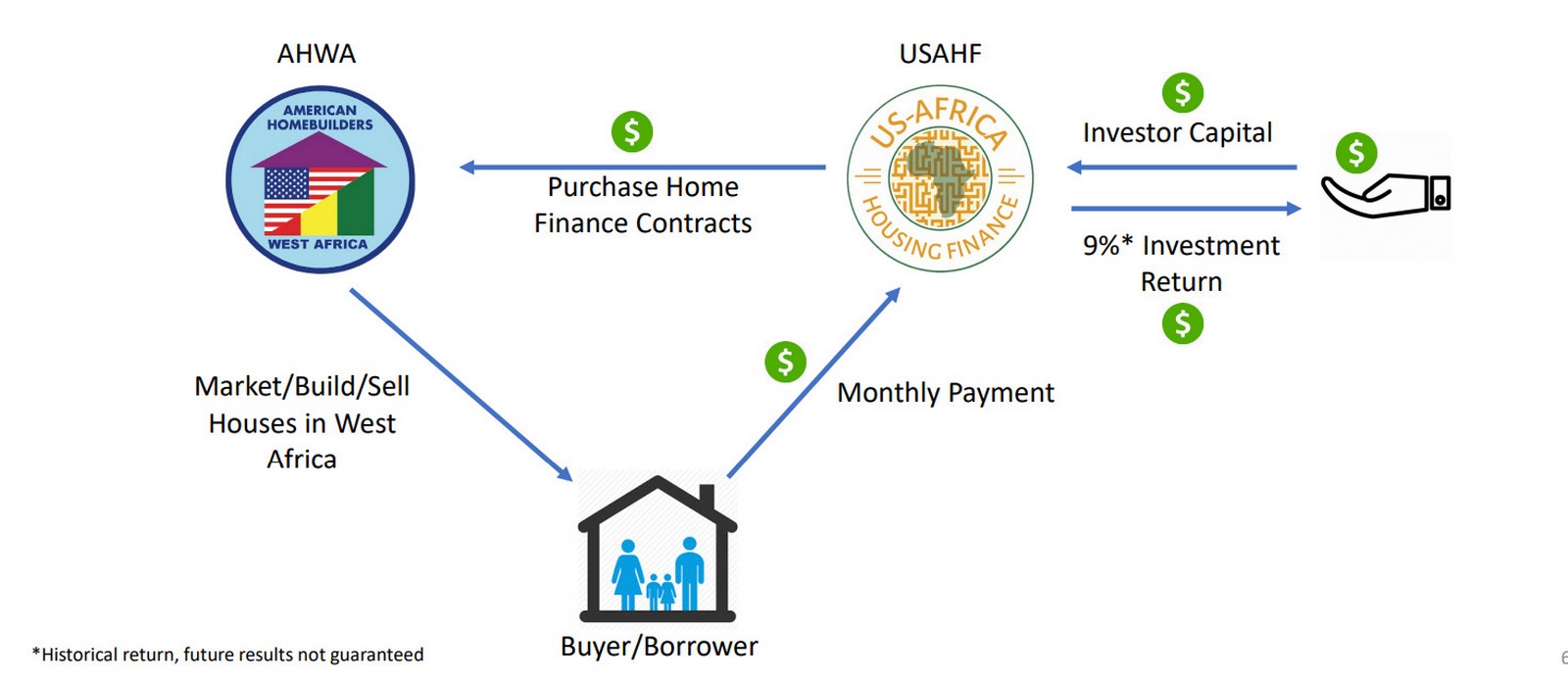

American Homebuilders of West Africa (AHWA) and US-Africa Housing Finance (USAHF) are US-registered limited liability companies collaborating to build, sell, and finance houses in West Africa. The relationship between the two firms is depicted in the figure below.

AHWA promotes, constructs, and sells homes in West Africa, while USAHF provides finance by acquiring AHWA-originating loans. Private investors fund USAHF (making an annual 9% return in US dollars over the previous three years), kicking off the virtuous cycle that drives this partnership ahead.

Another thing you will note is that there has been no government assistance or charity in this model to date. Both companies are for-profit (and are now profitable) and have depnded entirely on private funding raised in the United States. Having said that, there is a space for governments, foundations, or other quasi-governmental organizations to step in and give much-needed catalytic capital to help the respective firms go forward more rapidly and effectively. Since both firms’ business models have been proven, it is time for significant institutions to step up and assist.

Now, exactly how did these businesses overcome the four issues mentioned previously while others had failed? The first issue, low building quality, is not theoretically difficult to tackle because construction techniques are well understood in the United States, Europe, and other developed economies. However, doing so in a culture that accepts low quality as a “fact of life” necessitates investing in the local team’s growth and a great deal of effort and willingness to deliver a quality product. Fortunately, the co-founders of AHWA all share that aim, and as a result, they build houses that anybody would be happy to live in. Part of their zeal stems from their time as peace corps volunteers in Cote d’Ivoire in the 1990s. The instructions to the local Africans were given personally by the co-founder Jonathan Halloran on how to build a safer ladder, use power tools correctly, and establish a logistics depot as an indication of their devotion.

Jonathan believes that if you educate one group on how to do anything in an international-class manner, that group will enthusiastically pass on that knowledge to everyone who would listen. Fortunately, most Africans are willing to listen and learn because they want to see their country and continent grow.

Another issue is restricted economies of scale. Also, there is a lack of trust in developers, which is inextricably linked to the need for consumers to build their own houses and undergo the related anguish and sorrow if housing developers are trusted. Any member of the African diaspora will tell you a personal tale or one about a close friend or cousin who was “scammed” while attempting to build a house in Africa. AHWA has overcome the trust issue the old-fashioned way: they give a great product to their clients, and “word of mouth” has done the rest over time.AHWA is already a well-known brand in Guinea, West Africa, expanding into neighboring nations such as Sierra Leone, Côte d’Ivoire, and Senegal, with many more to follow.

The third issue is money, which is the most difficult. Giving a borrower a house loan is more complex than it appears. The apparent challenge is getting the funds to fund the loans (which is challenging enough when the target market is Africa), but the underwriting procedure may be more complicated. The lender cannot just lend to anybody; the borrower must be thoroughly verified through some systematic and repeatable method. This necessitates getting to know a potential borrower and analyzing the risk. To make this arduous effort easier, USAHF intends to first solely give loans to the African diaspora residing in OECD nations such as the United States, France, Canada, and the United Kingdom.

The combined AHWA/USAHF underwriting methodology is unique because it allows borrowers to pay monthly into an “escrow account” for up to 24 months to meet the 30% down payment requirement. This benefits the borrower and gives essential data and trust in the borrower’s capacity to pay. If someone has the financial discipline to make a monthly payment for a year or more without even owning a property, the chances of defaulting after owning the house are quite low. They are, in other words, a reasonable credit risk.

A well-developed method for dealing with the inevitable loan default is the final piece of the finance jigsaw. Regardless of how thorough your underwriting process is, certain defaults are unavoidable. Many bankers advise that if you don’t have any defaults, it shows your underwriting is too stringent, and you should relax the rules. AHWA and USAHF have an agreed-upon default mechanism and have successfully navigated it several times with minimal damage to either business or the borrower. Because of the massive demand for AHWA residences, resale has been reasonably straightforward, and values are likely to rise, protecting the defaulting borrower from severe losses.

Conclusion

Finally, both AHWA and USAHF have a viable, sustainable, and scalable plan that can alleviate Africa’s housing needs over time. To make this promise a reality, governments, DFIs, foundations, and other comparable organizations must step up and offer catalytic money.

References:

1.Africa Housing Finance (USAHF) | (no date) US. Available at: https://usafricahf.com/.

2.Dhillon, A. (2021) Solving the housing crisis in Africa, LinkedIn. Available at: https://www.linkedin.com/pulse/solving-housing-crisis-africa-ameet-dhillon/ .

3.Affordable housing (no date) Habitat For Humanity. Available at: https://www.habitat.org/emea/about/what-we-do/affordable-housing.